RSUs and PSUs – A Versatile Tool to Attract and Retain Executive Talent While Providing Unique Defer

There are many effective tax-planning tools for corporations who are looking to incentivize employees. Restricted Stock Units (RSUs) or Performance Stock Units (PSUs) have some unique characteristics, which make them preferable to actual stock, for many who are assembling executive compensation plans. As a result, companies are exploring the ability to expand their deferred compensation plans to include other forms of compensation that can effectively be deferred into the plan on a pre-tax basis, namely RSUs and PSUs.

Many companies now use RSUs with the potential for further tax deferral into their nonqualified deferred compensation (NQDC) plan. RSUs are not issued in the form of actual stock; rather they are notational shares that are measured and valued against the company’s stock.

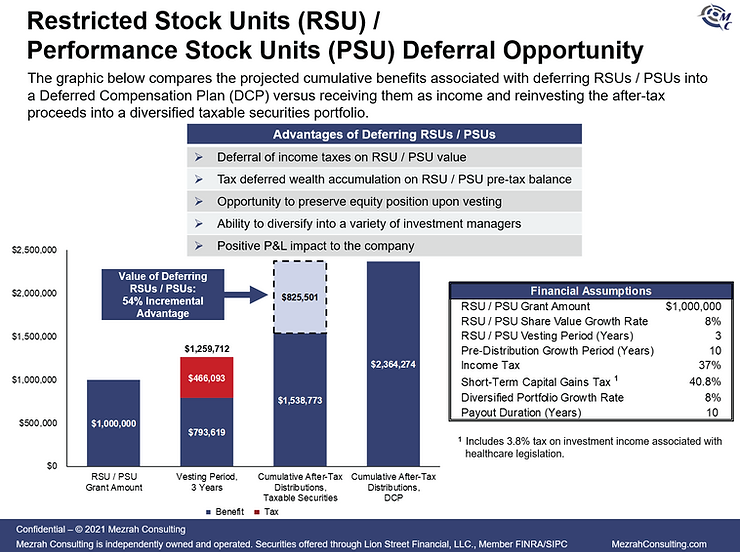

The company issues restricted stock units with similar restrictions as stock options, but the advantages are that the entire value and taxation of the units may be deferred to a future date without a §83(b) election. So instead of paying tax when the RSUs vest and placing the funds received in taxable securities, any units issued may continue to be deferred into an NQDC plan where the units’ value will grow without any current tax consequences to the employee. See Exhibit I below that displays the economic advantage of deferring RSUs.

However, many forms of equity compensation treated as “deferred compensation arrangements” must comply with an extensive and complicated section of the Internal Revenue Code.

Given IRC § 409A, there are two options for executives to defer RSUs into their deferred compensation plan:

-

Elect to defer RSUs before the grant has been made – prior to the grant of RSUs, a participant can elect to defer a percentage of their RSUs to be deferred until a future selected date (e.g. specific date, separation of service, or retirement).

-

Elect to defer RSUs that have not yet vested – for those RSUs that have been granted but not vested, a participant can elect to defer the non-vested RSUs at least 12 months prior to the RSUs’ vesting date and can then elect for them to be received at least 5 years from the date of vesting.

Both options provide an executive with the opportunity to diversify their current equity position within the company and invest a pre-tax amount of money that will then grow on a tax-favored basis. Alternatively, the deferred compensation plan may be structured to allow some or all of the deferred RSUs to be retained in the form of deferred stock if the company has minimum equity participation guidelines at the executive level. It is also possible to limit the deferral amount to only a portion of the RSUs if the company prefers executives to receive a portion of their vested shares.

With RSUs as part of an executive’s compensations plan and the need for advanced tax planning in this ever-changing economy, NQDC plans are a great benefit for both executives as well as the issuing companies. By utilizing the NQDC plan, the employee alleviates the tax-related issues associated with restricted stock and companies can create an attractive compensation package to recruit, retain and reward key executives within the organization. Specifically, RSUs can have a positive impact on a participant’s financial position while allowing them to more broadly diversify their net worth.

Careful planning with the assistance of a third-party administrator should ensure IRS compliance and well-executed executive plans. For more information about RSU and PSU deferral plans, please contact Mezrah Consulting.

Disclosure: This information is intended for educational purposes only and should not be construed as tax advice. You should talk with a tax professional before making any decisions.

More Information

For more information call (813) 367-1111 and ask for Sales, or email consulting@mezrahconsulting.com. A team member will reach out to you shortly!

Who We Are

Mezrah Consulting, based in Tampa, Florida, is a national executive benefits and compensation consulting firm specializing in plans for sizable publicly traded and

privately held companies. For more than 30 years, we have focused on the design, funding, implementation, securitization and administration of nonqualified executive benefit programs, and have advised more than 300 companies throughout the U.S.

As a knowledge-based and strategy-driven company, we offer clients highly creative

and innovative solutions by uncovering value and recognizing risks that other firms typically do not see. Custom nonqualified benefit plans are administered through our affiliate mapbenefits®, a proprietary cloud-based plan technology platform that provides enterprise plan administration for nonqualified plans, including reporting and functionality for plan participants and plan sponsors.