A nonqualified deferred compensation plan (DCP) is an executive benefit plan that allows...

Creating Pre-Tax Severance Benefits

When most people think about compensation, few think about severance as a form of compensation they will receive. It is important to plan for all contingencies regardless of their likelihood.

Severance from employment can occur for a variety of different reasons unrelated to your performance including a corporate change in control or ownership, a change in corporate leadership or just as a result of normal cost cutting. Severance benefits can make up a meaningful part of compensation that often is currently not needed.

-

Depending on the length of severance, it may not take long to find another opportunity thus creating unnecessary excess compensation and taxes.

-

Many may want to take time off upon separation but rarely does the time off last more than a few months.

-

There may be other forms of compensation that may vest, especially if one’s severance is the result of a change in control, the aggregate of which could result in excess parachute payments and excise taxes.

For these reasons, many executives may choose to defer their severance benefits (or part of their severance) into a non-qualified deferred compensation plan and warehouse that cash on a pre-tax basis to be distributed at a future point in time.

While severance is not always thought of as a traditional form of compensation, it can be included as a form of compensation that can be deferred. This is traditionally done through the “company contribution” provision within the plan that allows for the company to make discretionary contributions into the deferred compensation plan on behalf of the executive. When one is terminated from employment and severance is offered, the parties may agree to have some, or all of the severance paid in the form of a company contribution to the deferred compensation plan.

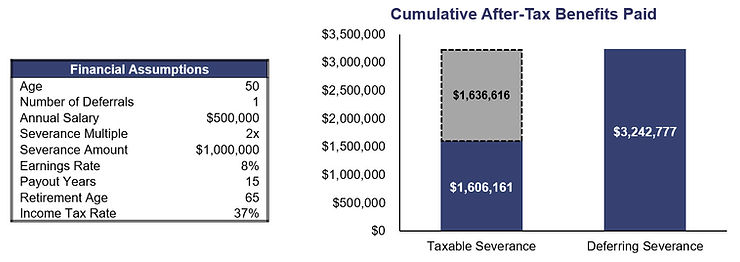

Hypothetical example for illustrative purposes only. Actual results will vary.

In the event of a change in control or ownership, 26 U.S. Code §280G limits the amount of compensation an executive can receive as a result of such change. In this situation, compensation (including severance) paid to the executive which exceeds three (3) times the executive’s gross income are considered “excess parachute payments.” Under 26 U.S. Code §4999, excess parachute payments are not deductible by the employer and the executive is subject to an additional 20% excise tax on these amounts.

How to Defer Severance

There are generally only three (3) ways one can defer severance:

-

In the original employment or severance agreement, the severance benefit or some percentage thereof is structured to be deferred;

-

If severance has not been offered yet in the form of a formal agreement or employment agreement;

-

If a current severance right exists at the time termination occurs, and the payout is scheduled to occur more than 12 months after termination. Simply stated, if a severance plan already exists and there is a legal obligation in place to pay severance within 12 months after termination, then it is generally too late to defer the severance.

Planning is paramount when including severance in one’s employment agreement; either severance needs to be elected to be deferred prior to a formal agreement going into place or the severance payments need to be designed to be delayed for at least 12 months after termination to allow the participant to make a deferral election at the time of termination. This delay can allow one to accommodate IRC 409A by making an election to defer severance 12 months prior to the date it is scheduled to be received. This will only be permitted if the executive defers the income for at least five (5) years from the date they would have otherwise received the income.

In the event of a change in control or ownership, there are several ways to reduce the impact of severance agreements under 26 U.S. Code §280G. Traditionally, severance paid as a result of termination upon a change in control are included in the calculation of excess parachute payments. However, severance agreements can be amended and/or modified to reclassify such payments as reasonable compensation effectively removing them from the calculation of excess parachute payments, if they are put in place at least one (1) year prior to a change in control or ownership. Below are four (4) different ways to reposition severance benefits to avoid the negative tax impacts of §280G:

-

Restructure the agreement so that normal severance only applies to a termination prior to or more than 24 months after a change in control, and cap severance payments within 24 months of a change in control at the three (3) times gross pay limit when combined with other severance payments;

-

Restructure all or parts of severance amounts that might otherwise be payable as severance as a company contribution allocated to the deferred compensation plan with appropriate vesting during employment;

-

Recharacterize severance as reasonable compensation for personal services over a period of time after a change in control;

-

Recharacterize severance as a payment for adhering to an enforceable non-compete agreement.

If severance has not yet been offered, then one can elect to defer all or part of their severance prior to entering into a binding agreement to receive it. Having the ability to make a planning decision ahead of time could save an executive a significant amount of unnecessary taxes and provide him or her with an opportunity to accumulate wealth on a pre-tax basis for retirement purposes. If the income is not needed due to another job already being secured or the release of other types of income, deferring severance benefits can make a lot of sense from an overall financial planning perspective.

More Information

For more information call (813) 367-1111 and ask for Sales, or email consulting@mezrahconsulting.com. A team member will reach out to you shortly!

Who We Are

Mezrah Consulting, based in Tampa, Florida, is a national executive benefits and compensation consulting firm specializing in plans for sizable publicly traded and

privately held companies. For more than 30 years, we have focused on the design, funding, implementation, securitization and administration of nonqualified executive benefit programs, and have advised more than 300 companies throughout the U.S.

As a knowledge-based and strategy-driven company, we offer clients highly creative

and innovative solutions by uncovering value and recognizing risks that other firms typically do not see. Custom nonqualified benefit plans are administered through our affiliate mapbenefits®, a proprietary cloud-based plan technology platform that provides enterprise plan administration for nonqualified plans, including reporting and functionality for plan participants and plan sponsors.